MERCURY: Market Microstructure Simulation Lab

Overview

MERCURY is a research-grade market microstructure simulator built as a full system rather than a notebook demo. At its core is a continuous double auction with price-time priority, a realistic limit order book, heterogeneous agent behavior, endogenous price formation, and explicit stress propagation. Around that core, I built benchmark suites, parameter sweeps, publication-grade plots, and a reproducible reporting pipeline so the project can function as both a simulator and a research artifact.

What I Did

- Architected the exchange core with limit-order-book mechanics, partial fills, cancels, replace logic, iceberg orders, pegged orders, and maker-taker accounting.

- Designed heterogeneous agents for market making, momentum, arbitrage, execution, panic selling, stop-loss cascades, spoofing, and venue arbitrage.

- Added market-structure experiments for flash crashes, cross-asset spillovers, fragmented venues, liquidity withdrawal, and regulation controls such as circuit breakers.

- Built benchmark, sweep, plotting, and report-generation workflows so the system can run scenario families and publish polished outputs automatically.

- Validated the platform with an automated test suite covering matching logic, metrics, reporting, and visualization workflows.

Results/Impact

- Benchmarked 18 built-in scenarios spanning baseline trading, flash-crash dynamics, cross-asset spillovers, fragmented venues, and fee economics.

- Reached 67 passing tests across the simulator core, benchmark tooling, and reporting pipeline.

- Reduced flash-crash fragility from 54.7493 to 21.0714 and crash detections from 45 to 9 when circuit breakers were enabled.

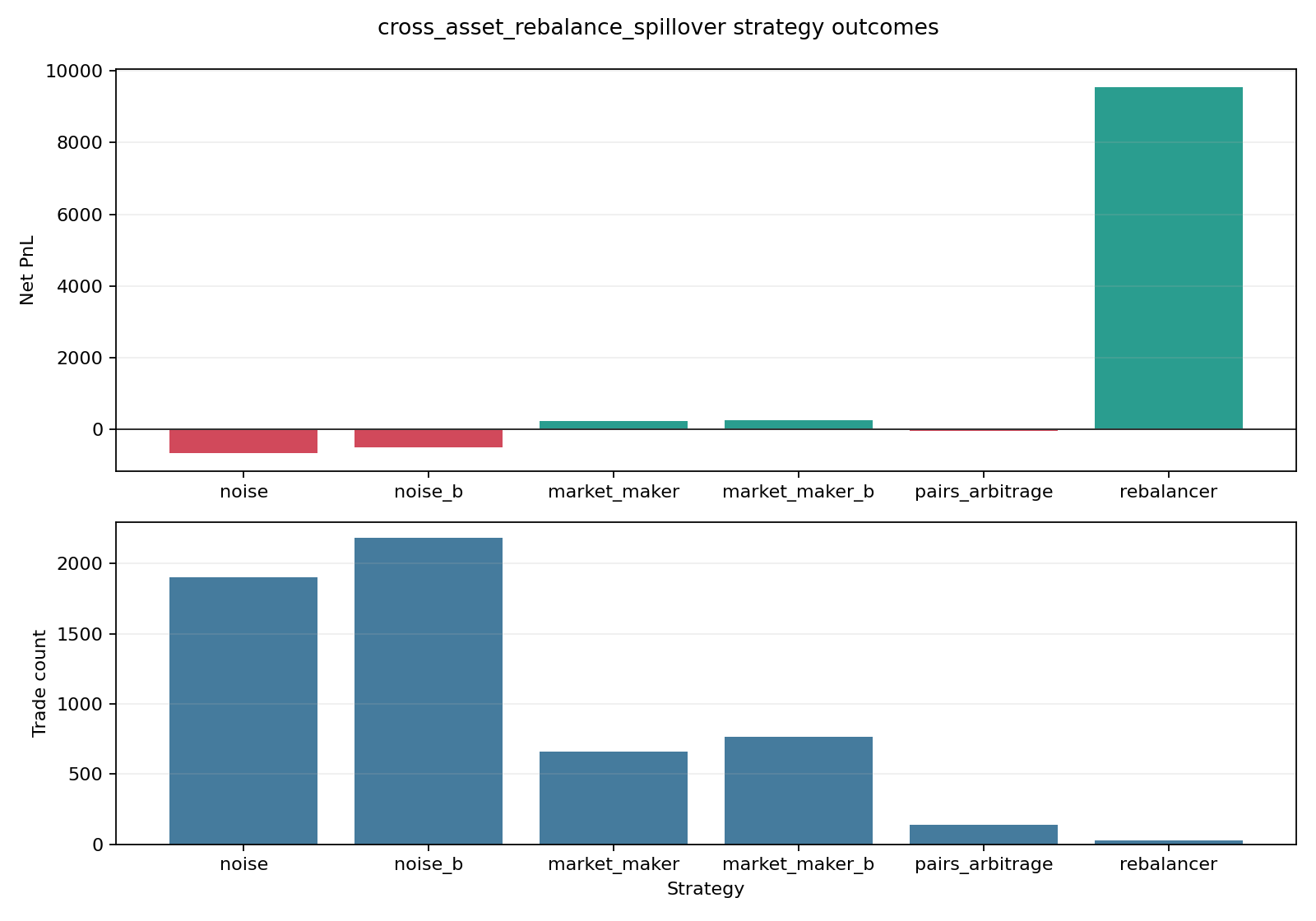

- Captured mean cross-asset dislocation of 0.8201 and rebalancer net PnL of 9549.0 in spillover experiments.

- Measured crossed-market frequency of 0.0966 and mean crossed width of 0.9134 in fragmented-venue benchmarks.

Tech Stack

- Python, Agent-Based Simulation, Market Microstructure, Continuous Double Auction, Limit Order Books, Matplotlib, Pytest, YAML, Quarto, Reproducible Research Tooling

Deliverables

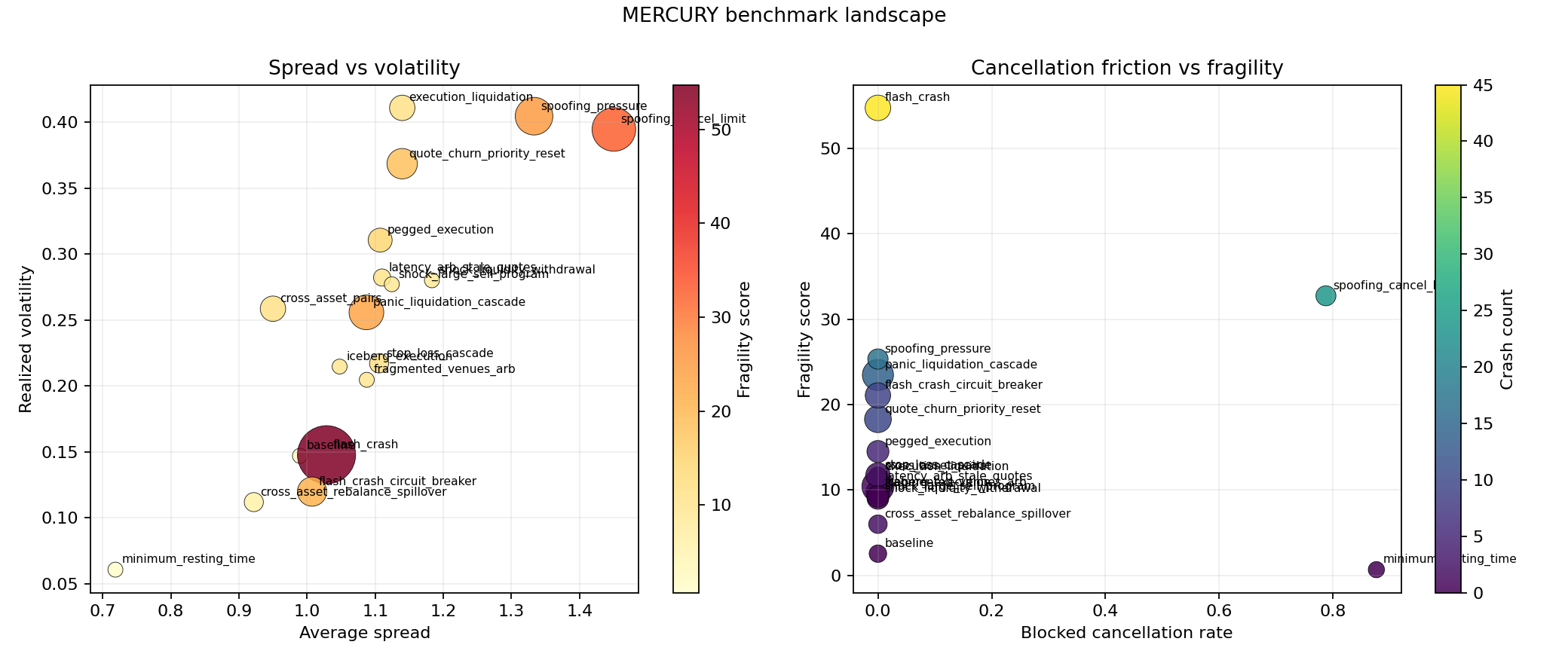

Benchmark Landscape

The benchmark layer turns the simulator into a decision surface instead of a single scenario demo. It makes spread, volatility, fragility, crash intensity, and venue economics visible across a consistent scenario family.

Benchmark landscape. Spread, volatility, fragility, and crash intensity are mapped together so unstable regimes separate cleanly from merely active ones.

Benchmark landscape. Spread, volatility, fragility, and crash intensity are mapped together so unstable regimes separate cleanly from merely active ones.

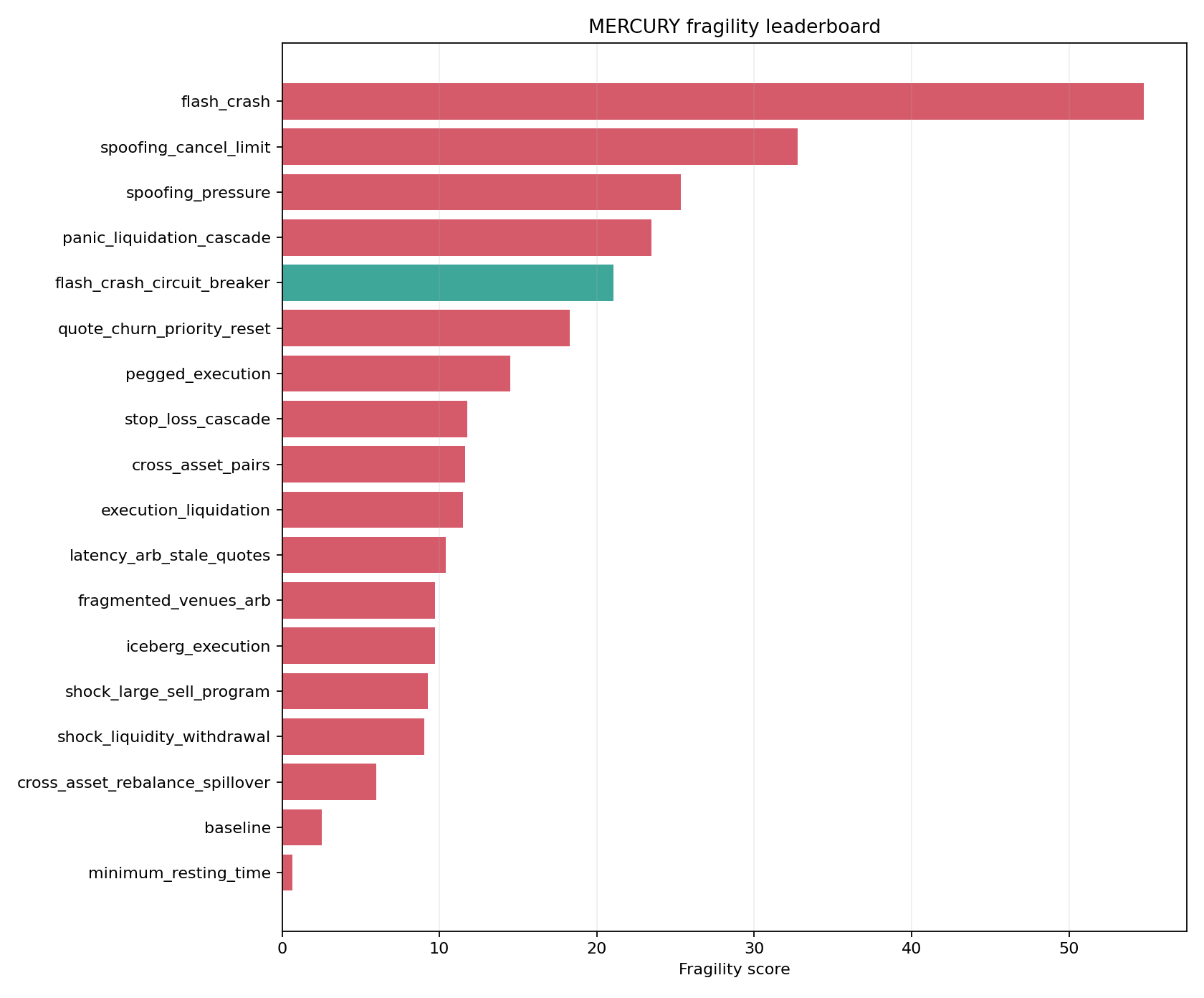

Fragility leaderboard. The stress ranking makes it immediately clear which market structures become brittle under pressure.

Fragility leaderboard. The stress ranking makes it immediately clear which market structures become brittle under pressure.

Fee economics. Maker rebates, taker fees, and net exchange revenue are measured directly instead of being treated as background assumptions.

Fee economics. Maker rebates, taker fees, and net exchange revenue are measured directly instead of being treated as background assumptions.

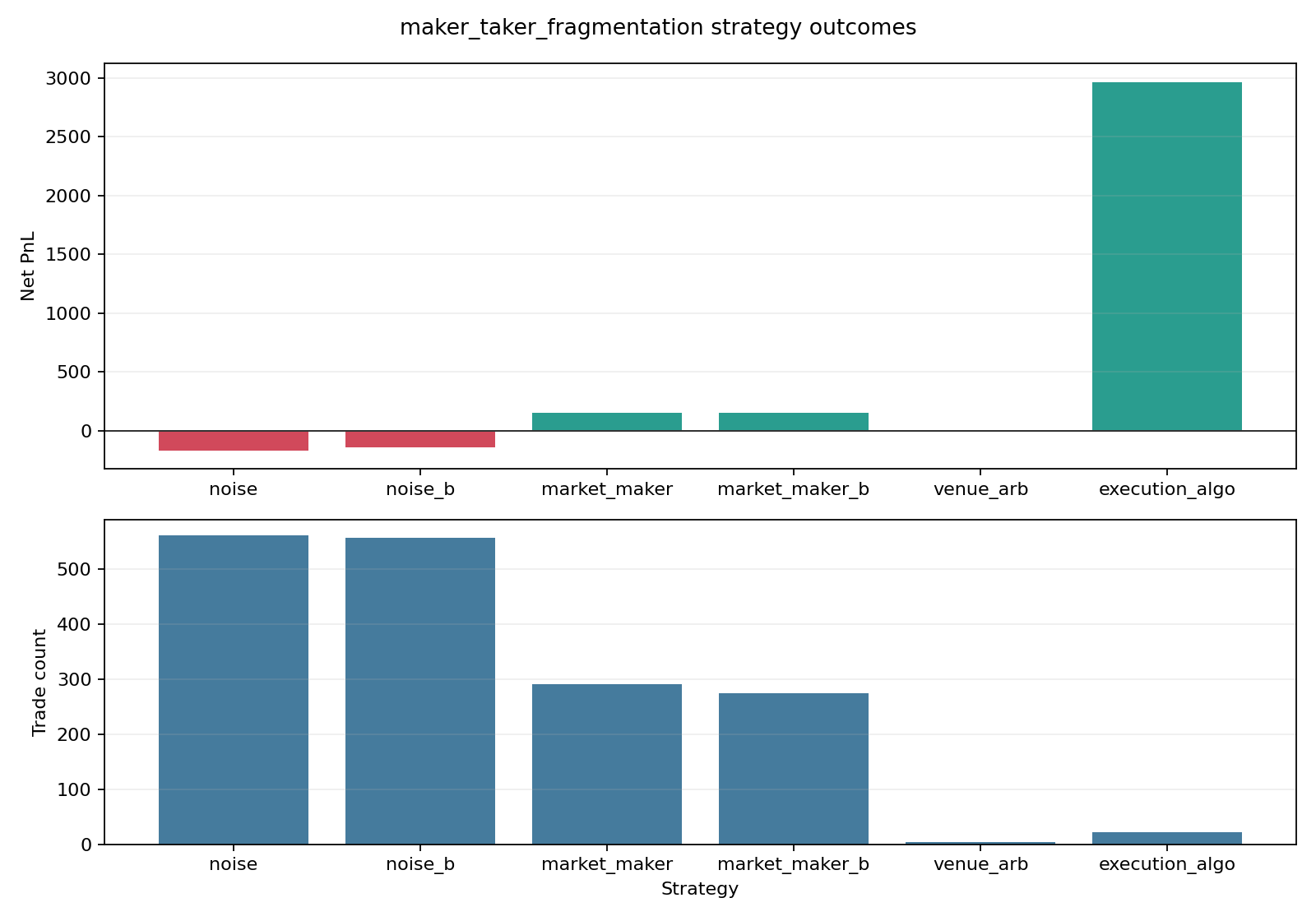

Strategy PnL under fees. Venue economics materially change routing incentives and who wins under fragmented liquidity.

Strategy PnL under fees. Venue economics materially change routing incentives and who wins under fragmented liquidity.

Signature Experiments

Flash Crash Formation

MERCURY can generate endogenous crash behavior from interacting strategies and liquidity conditions rather than relying on a simple exogenous price drop. That is the difference between a price toy and a market-structure lab.

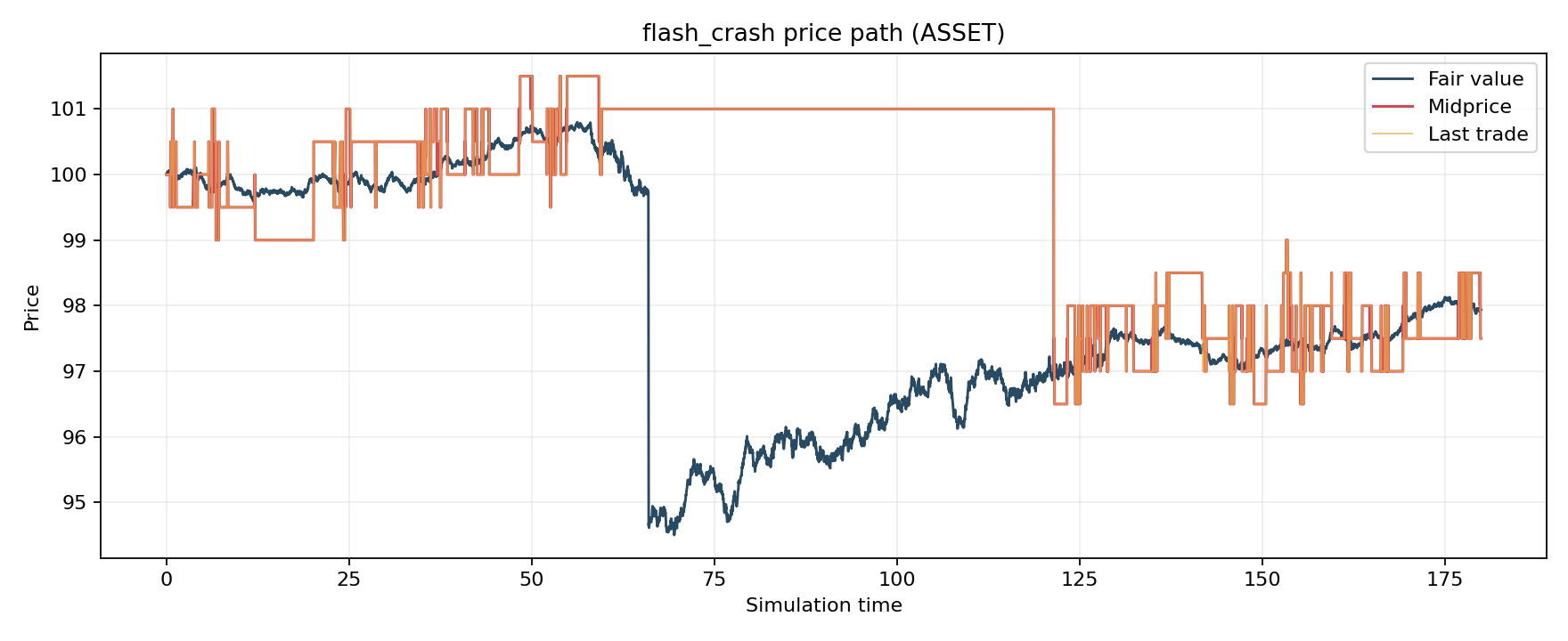

Price path under stress. Crash formation emerges from order flow, liquidity withdrawal, and feedback loops inside the book.

Price path under stress. Crash formation emerges from order flow, liquidity withdrawal, and feedback loops inside the book.

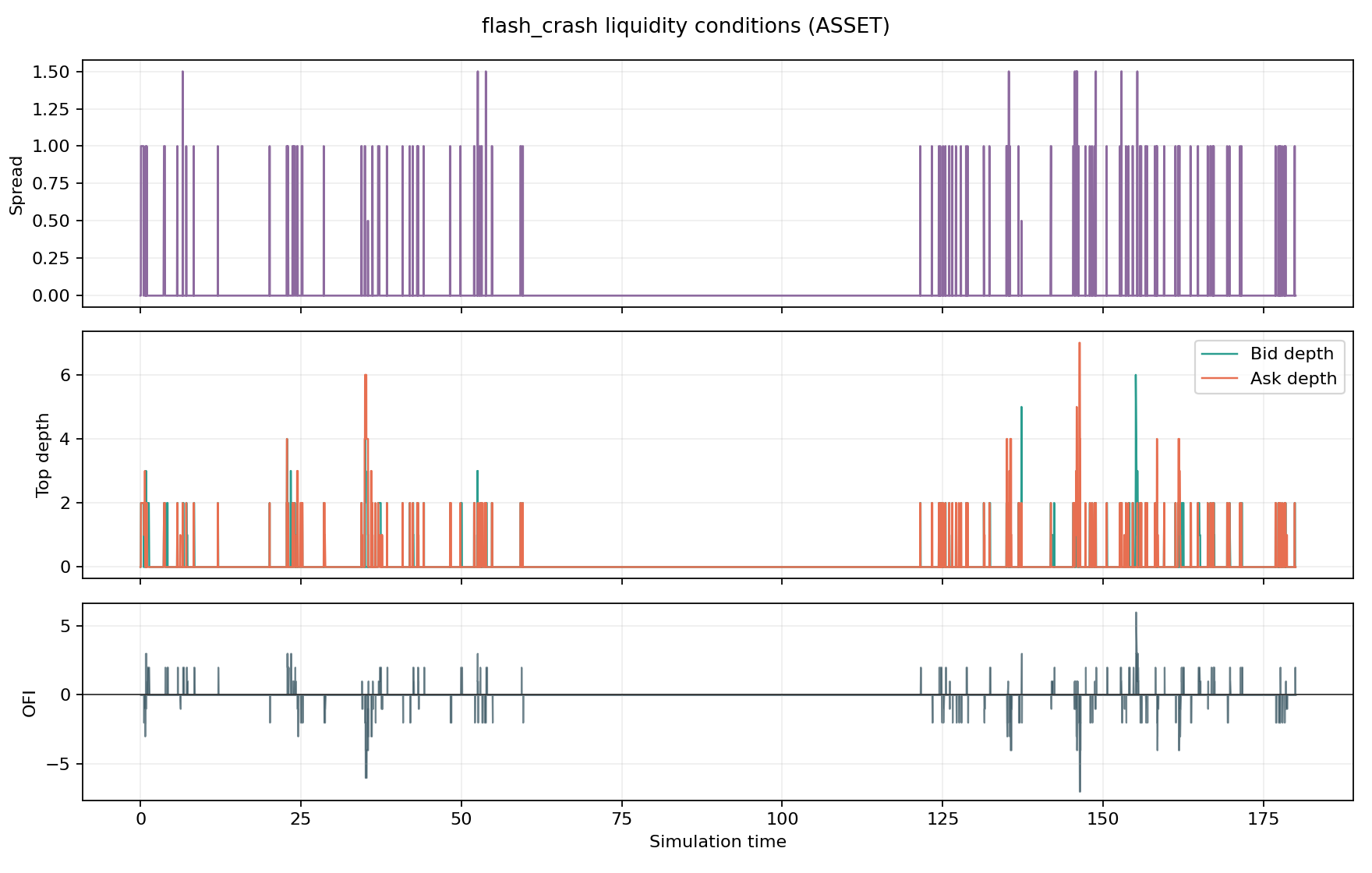

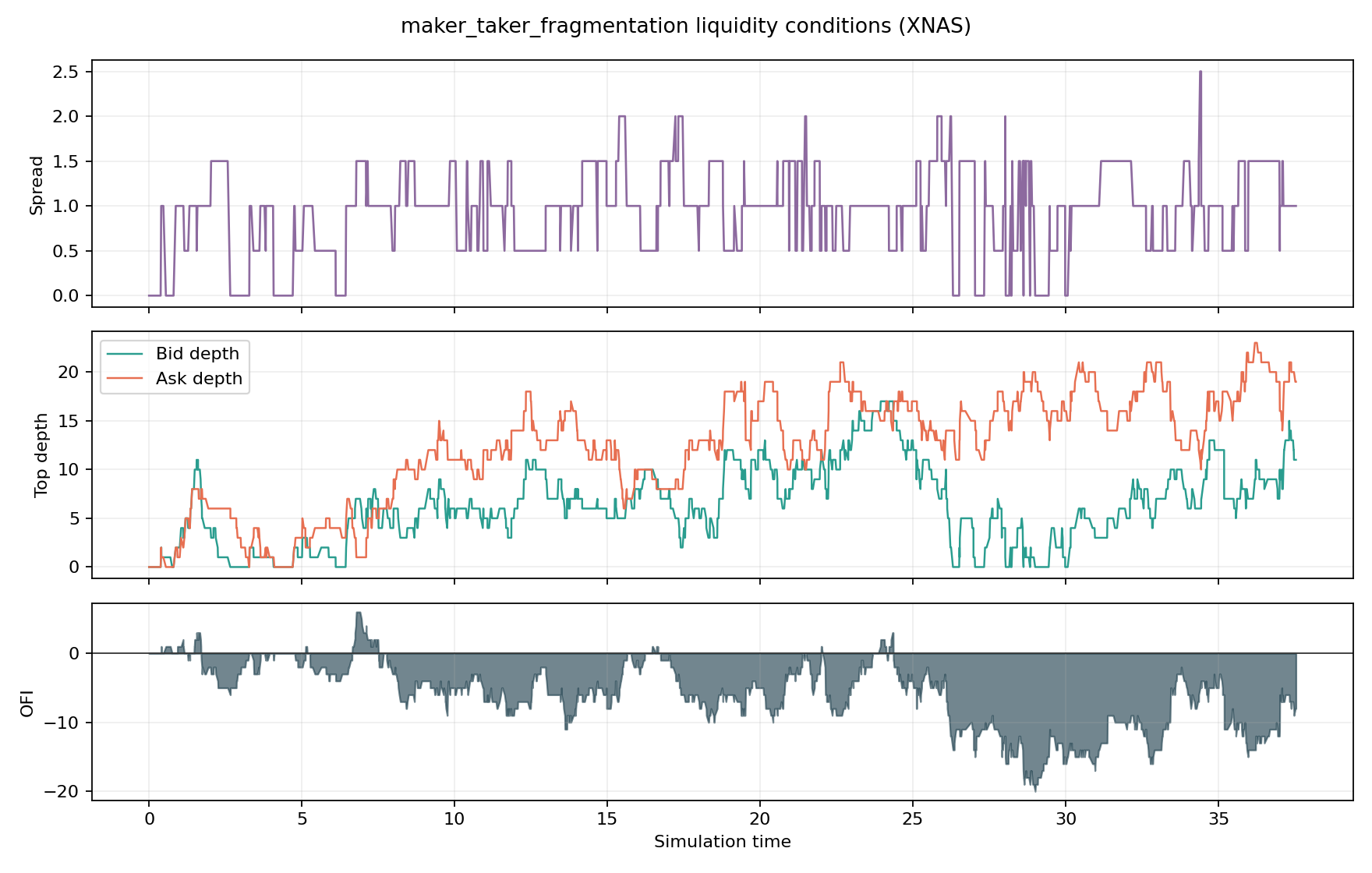

Liquidity conditions. Spreads widen and displayed depth thins rapidly once the market moves into a fragile regime.

Liquidity conditions. Spreads widen and displayed depth thins rapidly once the market moves into a fragile regime.

Cross-Asset Spillovers

The simulator is not confined to a single order book. It supports correlated assets, cross-asset fair values, pairs logic, and institutional rebalancing so spillovers can be modeled directly.

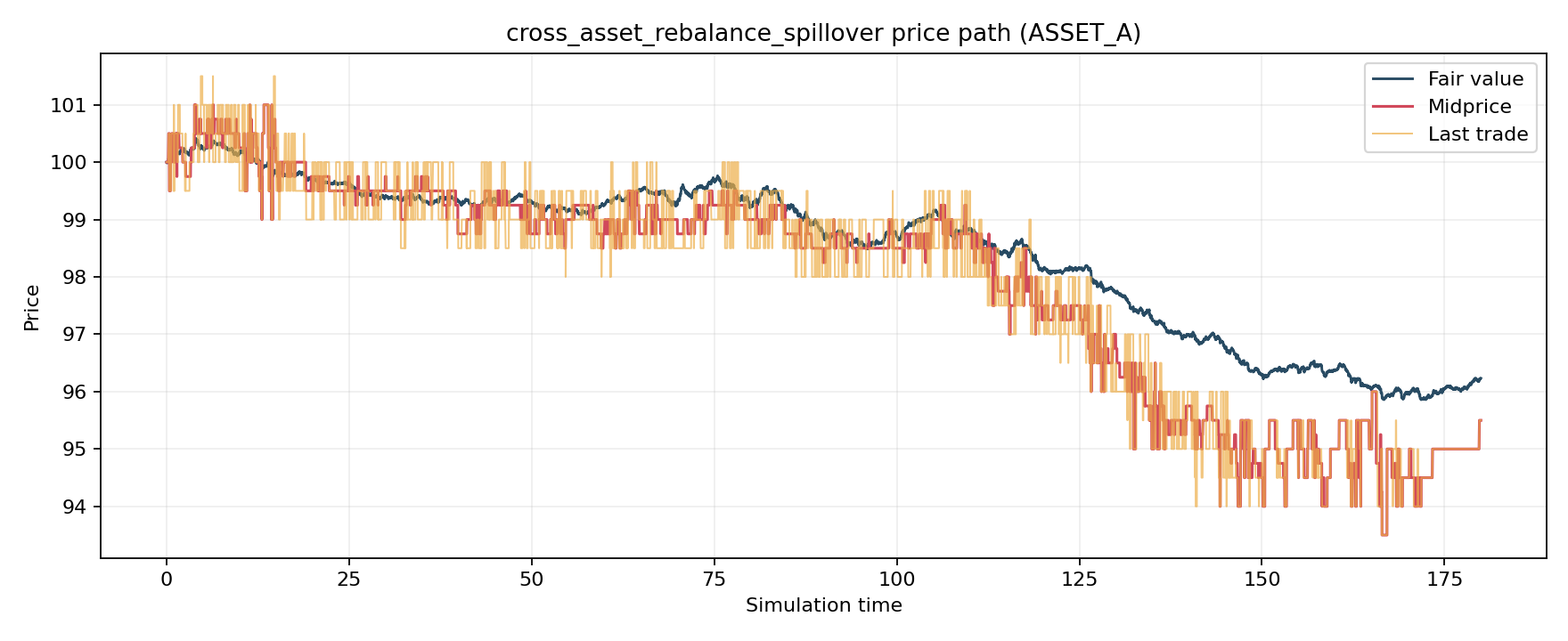

Cross-asset price path. Spillovers propagate across linked assets rather than remaining isolated to one venue.

Cross-asset price path. Spillovers propagate across linked assets rather than remaining isolated to one venue.

Cross-asset strategy PnL. Rebalancing and arbitrage behavior become measurable outputs instead of assumed narratives.

Cross-asset strategy PnL. Rebalancing and arbitrage behavior become measurable outputs instead of assumed narratives.

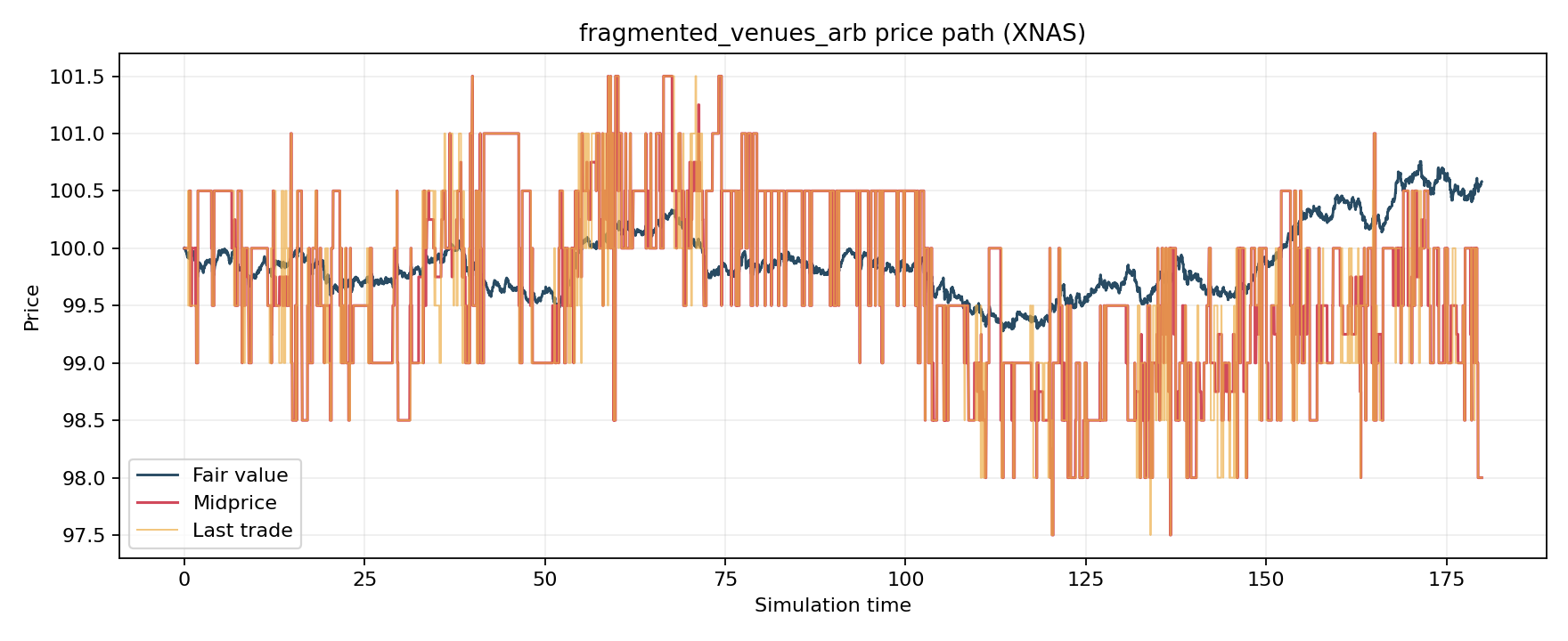

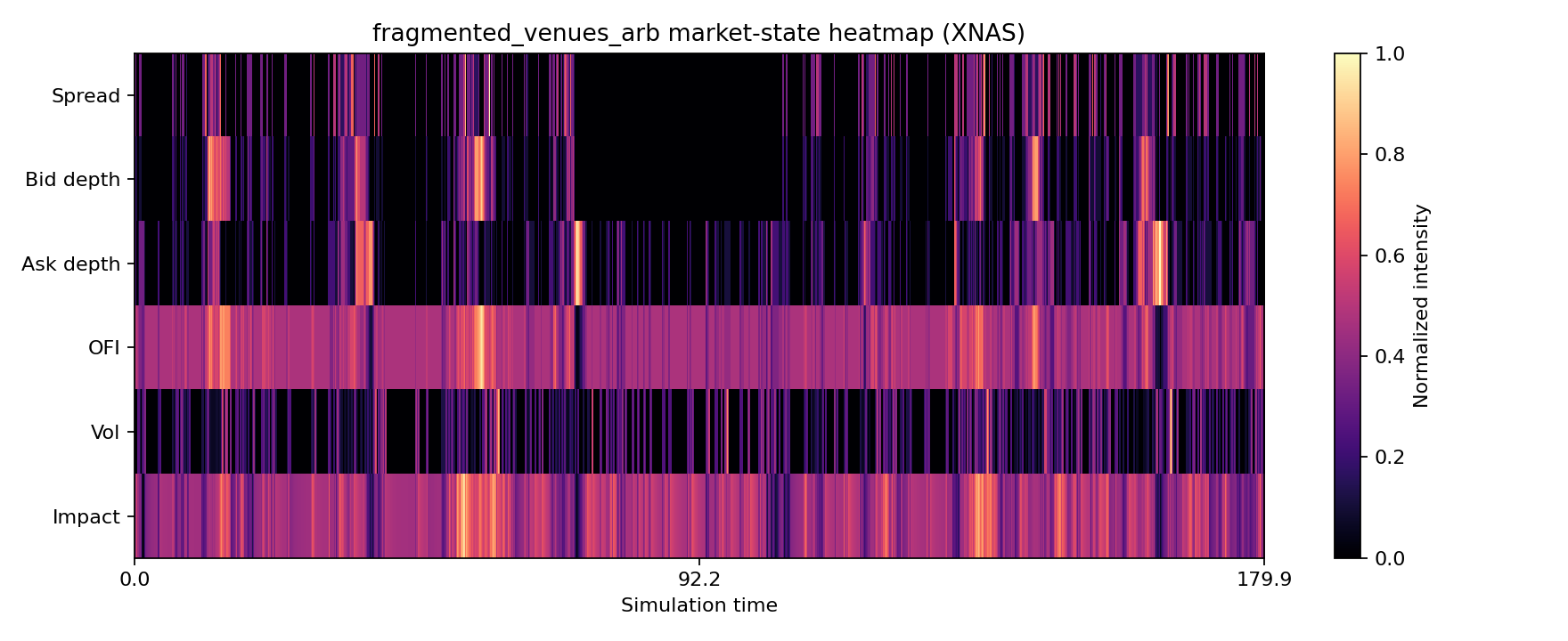

Fragmented Venues And Repair

MERCURY can reinterpret multi-asset infrastructure as fragmented venues for the same underlying. That makes crossed markets, best-execution pressure, and venue arbitrage observable instead of hand-waved.

Fragmented venues. The price-path view shows how dislocations open and get repaired when venues compete for flow.

Fragmented venues. The price-path view shows how dislocations open and get repaired when venues compete for flow.

Market-state heatmap. Fragmentation is visible as a structural pattern, not just a line on a chart.

Market-state heatmap. Fragmentation is visible as a structural pattern, not just a line on a chart.

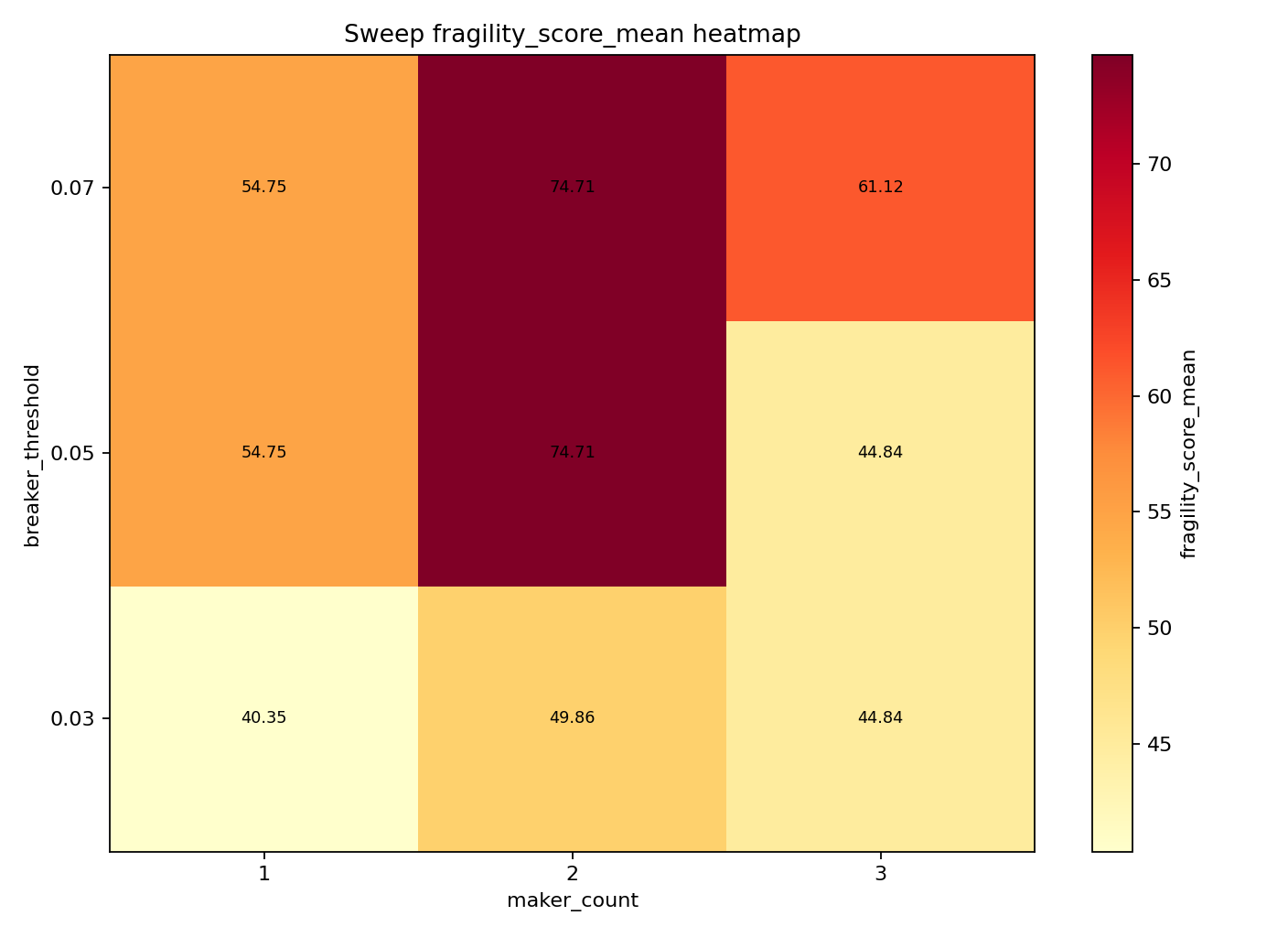

Research Workflow

The project is stronger because it does not stop at simulation. It can run benchmark families, sweep parameters, rank cases by an objective metric, and publish a reproducible report bundle that others can inspect without rebuilding the environment from scratch.

Sweep objective. The research workflow tracks fragility directly and compares scenario families against the target metric.

Sweep objective. The research workflow tracks fragility directly and compares scenario families against the target metric.

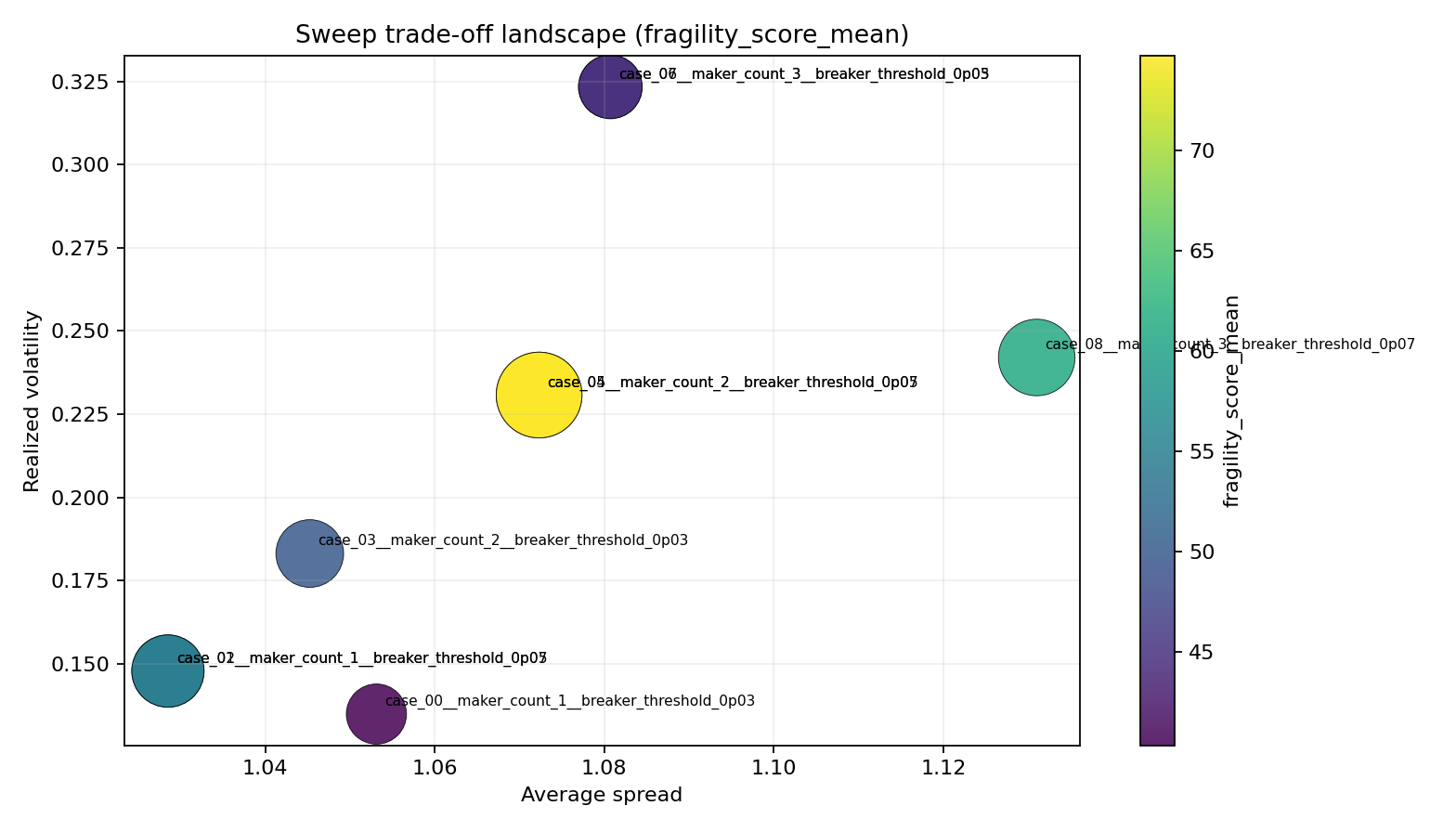

Tradeoff surface. Parameter changes are evaluated as explicit tradeoffs rather than isolated wins.

Tradeoff surface. Parameter changes are evaluated as explicit tradeoffs rather than isolated wins.

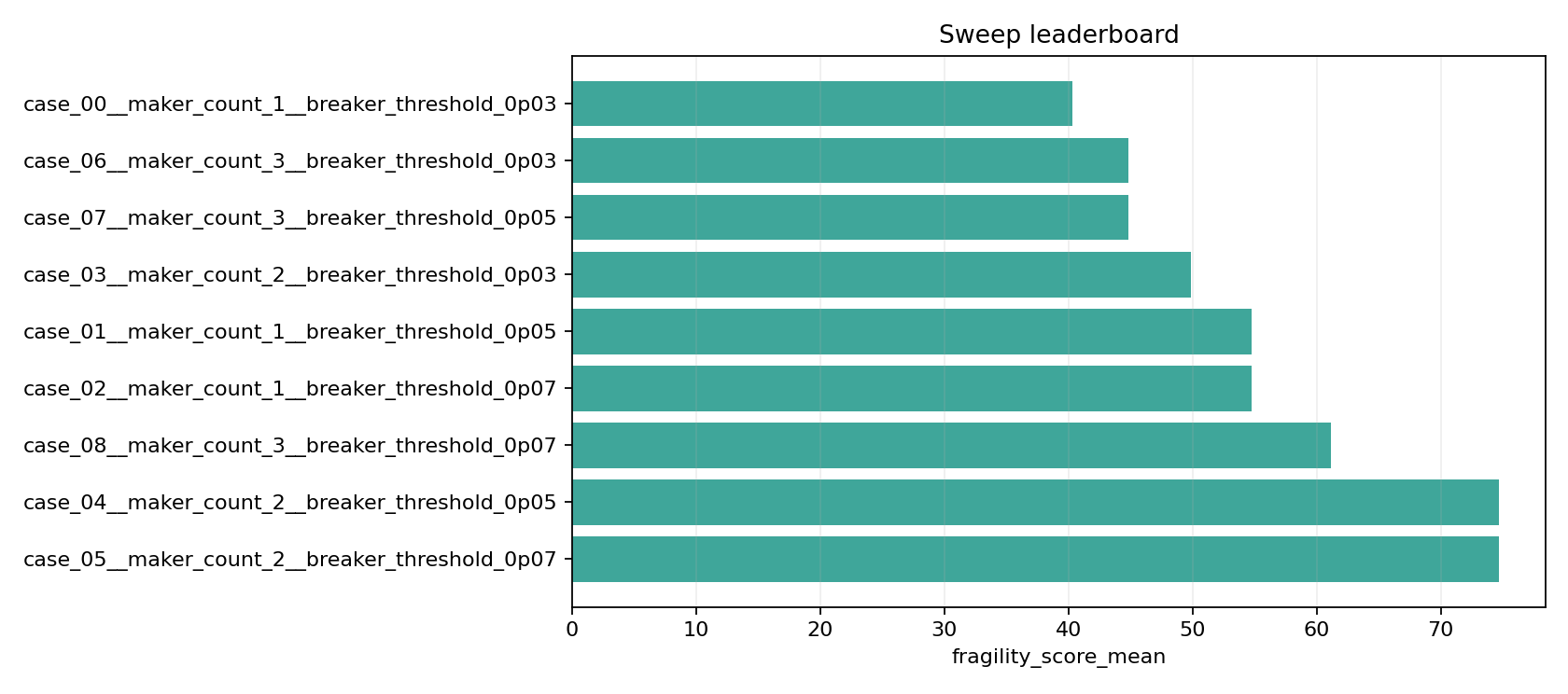

Sweep leaderboard. Best and worst cases are ranked automatically, which makes parameter tuning auditable and repeatable.

Sweep leaderboard. Best and worst cases are ranked automatically, which makes parameter tuning auditable and repeatable.

Liquidity response. The platform captures how fee structures and participant behavior reshape depth and market quality.

Liquidity response. The platform captures how fee structures and participant behavior reshape depth and market quality.

Why This Project Matters

MERCURY is the kind of work that signals systems thinking, modeling discipline, and software engineering at the same time. It is not a dashboard layer looking for a story. It is an actual simulation and research platform with outputs that can support discussion about stability, regulation, and market design.